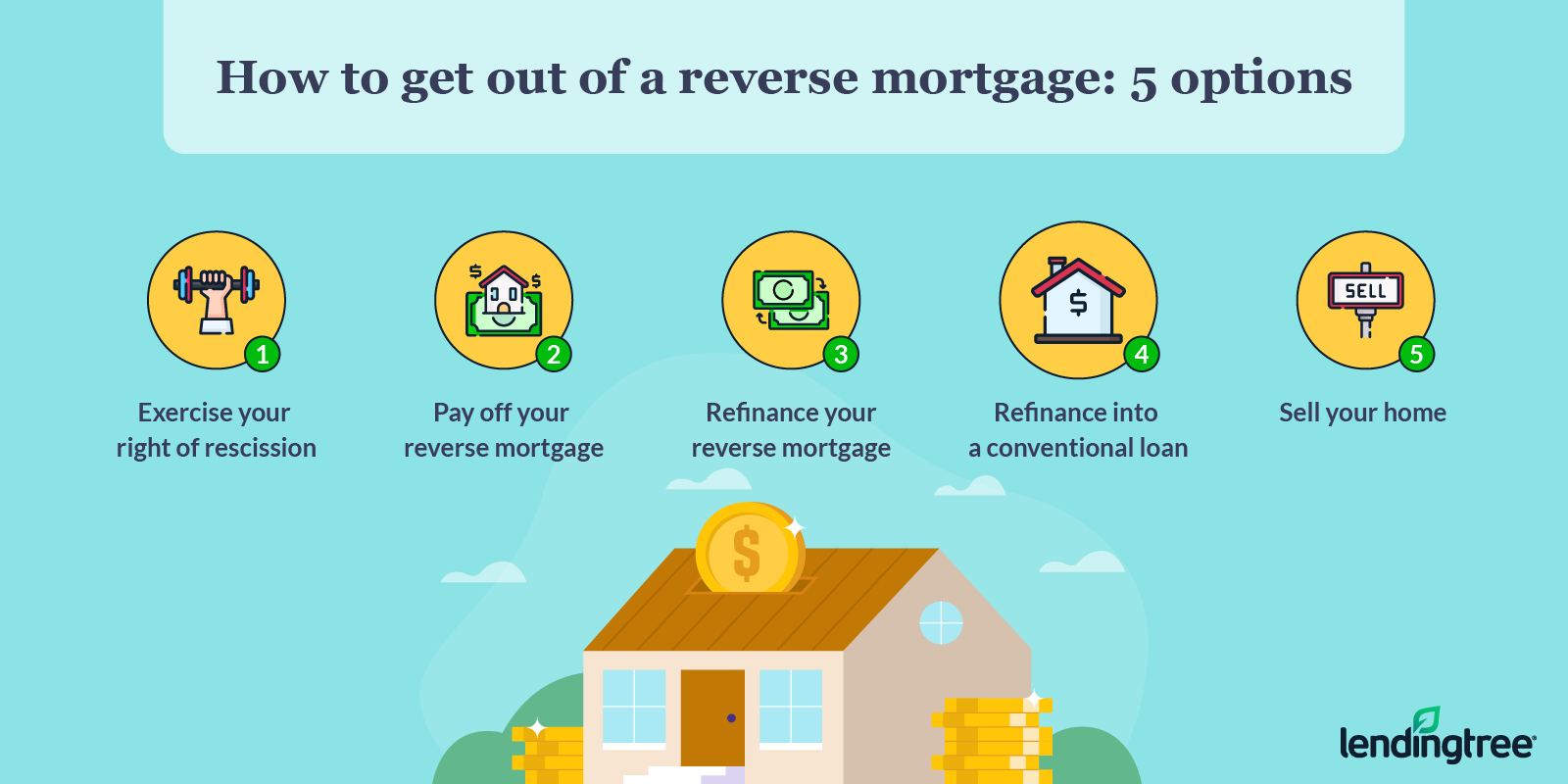

Nonetheless, if you promote the financing responsibilities noted above, your reverse home loan will certainly not come due till the last customer vacates the house or passes away. When this happens, the home is marketed, as well as the profits of the sale are made use of to pay the car loan balance in full. If successors desire to maintain the house, they can refinance the reverse home mortgage right into a conventional lending. They will certainly require to pay either the loan balance or 95% of the evaluated worth, whichever is lower. After repaying your existing home mortgage, your reverse mortgage lending institution will pay you any type of remaining profits from your brand-new car loan. If you own your residence cost-free as well as clear, you'll obtain every one of the proceeds from the lending given that you don't have a home loan equilibrium to settle initially.

Though, you might be able to transform your settlement choice in the future for a fee. Just like a bank loan, a reverse home loan allows you to access your house equity in the form of a round figure, a line of credit-- or perhaps a dealt with regular monthly settlement. If you're a house owner aged 60 as well as over, a reverse home loan is one way that you may have the ability to leverage the equity in your house to accessibility added cash money. This is not something all lenders supply-- Westpac does not for instance-- however there are various other methods to access the equity in your house which might be preferable for your scenario.

Getting money from your home mortgage might appear also good to be true. After all, if you haven't ended up paying your home loan and also you aren't selling your house, where is the money coming from? The quantity you receive relies on added variables which likewise include your age, interest rates and whether you're trying to find a settlement for life or for an established term. My idea would be that you ask for a proposal for your details scenarios. It's cost-free, it has no responsibilities and we can send you one with no stress.

In addition to this very first repayment, you can get future funds as required with the alternatives below. " Single-use" reverse mortgages, additionally called "credit fundings," are need-based finances for an unique function, such as making property tax repayments or paying for residence fixings. Generally, single-purpose reverse home loans can just be used to make property tax payments or spend for residence fixings. As well as because they're not regulated or guaranteed by the government, they can attract home owners in with assurances of greater loan quantities-- however with the catch of a lot higher rates of interest than those government guaranteed reverse home loans. You repay your finance when you move out of your house, sell it or the last debtor passes away. This suggests you do not need to make any payments on a reverse home loan until the finance is due.

- However since the cash from a single-purpose reverse home loan needs to be used in a details way, they're generally much smaller in their quantity than HECM financings or proprietary reverse mortgages.

- With plenty of people requiring help and also couple of home mortgage providers providing, Pete discovered terrific success in going the extra mile to find home mortgages for people whom many others thought about shed reasons.

- While reverse mortgages provide elders accessibility to large amounts of cash, keep in mind, this suggests they 'd be obtaining against their residence-- indicating they 'd lose your house if something went wrong.

- As the homeowner, you are in charge of your taxes, insurance policy, as well daily finance group as any type of other analyses on your home (i.e. HOA dues if any).

- These costs can be obtained of the lending amount, so you do not have to pay them expense, but they will reduce how much money you obtain after closing.

For additional information on how the FTC manages information that we accumulate, please read our personal privacy plan. The FTC as well as its police partners revealed actions against numerous revenue frauds that tricked people out of numerous millions of bucks by wrongly informing them they might make a great deal of cash. One of those rip-offs was 8 Number Dream Lifestyle, which touted a "proven company version" and told ... Money of America can help you obtain the best terms out of your Opposite Mortgage loan.

If you sell or move title to the property and also no other debtor preserves title to the residence or maintains a leasehold that satisfies particular conditions, the lending institution might call the finance due. An additional kind of available reverse home mortgage, which isn't federally guaranteed, is called a "proprietary" reverse home mortgage. All of a sudden, you have actually drawn that Look at more info last reverse home loan settlement, and after that the next tax obligation expense comes around. And also considering that a reverse home loan is only allowing you tap into a portion of the worth of your house anyway, what happens as soon as you reach that limitation? Yet even after that, you're not mosting likely to obtain the complete percentage you receive. Due to the fact that there are fees to pay, which leads us to our following point.

Keep Your Beneficiaries Notified

Before obtaining a reverse home loan, you should initially pay off and also shut any outstanding finances or credit lines that are safeguarded by your house. You can utilize the money you receive from a reverse home mortgage to do this. Don't forget that although a reverse mortgage can offer you with a line of credit, you are still in charge of various other living costs like taxes and also insurance coverage. Home Equity Conversion Mortgages represent 90% of all reverse home mortgages came from the U.S . As of 2006, the number of HECM home loans that HUD is accredited to insure under the reverse home loan legislation was covered at 275,000.

Purchase A House With An Agent Who Offers, Not Sells

Although commonly readily available, HECMs are only offered by Federal Real estate Administration -accepted loan providers, and also before closing, all borrowers should obtain HUD-approved counseling. There are different kinds of reverse mortgages, and also each one fits a various financial demand. A reverse mortgage is a means for property owners ages 62 and older to utilize the equity in their residence. With a reverse home loan, a property owner who has their house outright-- or a minimum of has substantial equity to attract from-- can take out a portion of their equity without having to repay it till they leave the home.

Just How Much Can You Borrow With A Reverse Home Mortgage?

A reverse home loan initial primary limitation is the quantity of money a reverse home mortgage consumer can obtain from the lending. As a reverse home loan customer, you are called for to stay in the home and also preserve it. If the home falls under disrepair, it won't be worth fair market value when it's time to sell, and the loan provider will not be able to recoup the total that it has included the debtor. The profits that you'll obtain from a reverse mortgage will certainly depend on the lending institution and your layaway plan. The United State Department of Housing and Urban Advancement needs all prospective reverse home loan customers to complete a HUD-approved therapy session.

Certainly, similar to among these financings, a reverse home mortgage can give a round figure or a credit line that you can access as required, based upon how much of your house you have actually settled as well as your sample letter to cancel timeshare contract home's market price. However unlike a residence equity loan or a HELOC, you do not need to have a revenue or great credit rating to certify, as well as you will not make any kind of loan repayments while you inhabit the residence as your key house. Just like a forward mortgage, the house is the collateral for a reverse home mortgage. When the homeowner moves or passes away, the earnings from the house's sale most likely to the loan provider to repay the reverse home mortgage's principal, rate of interest, mortgage insurance, and also fees.